With interest rates at all-time lows, investors have to think about which stocks can provide them with long-term income streams.

Thankfully, in Singapore, there are lots of dividend stocks to choose from that provide us with steady payments.

However, we should also buy dividend stocks that have sustainable growth. Crucially, that means dividends that continually (and reliably) grow year after year.

That gives investors a measure of sustainability of dividend payments. Here are three Singapore dividend stocks that long-term, buy-and-hold investors can consider adding to their portfolios.

1. DBS Group

Leading Singapore bank DBS Group Holding Ltd (SGX: D05) is a staple of the Singapore stock market. It’s no surprise that the banking group is also Singapore’s largest company by market capitalisation.

Seen as a reliable bank stock, it also pays a reliable dividend. However, to fund any dividend, a company must have solid financials that allow it to pay shareholders.

DBS has that. Even during this pandemic year, its fundamentals have remained relatively strong amid the headwinds. For the first nine months of 2020, its total income actually hit a record high of S$11.3 billion.

Yet because of provisions made for potential non-performing loans, its net profit fell during the period. That still didn’t stop DBS from boasting a CET-1 capital ratio of 13.9%, which was well above regulatory requirements.

As for the bank’s dividend, from 2009-2019 DBS grew its DPS from S$0.56 to S$1.23. That’s equal to a compound annual growth rate (CAGR) of an impressive 8.2%.

Although the bank has had to cap its dividend this year (meaning a yield below 3%) due to restrictions imposed by the Monetary Authority of Singapore (MAS), DBS will likely resume paying a substantially higher dividend in 2021.

2. Keppel DC REIT

Second on the list is data centre-focused real estate investment trust (REIT) Keppel DC REIT (SGX: AJBU). The REIT does what it says on the tin; it leases out data centre properties in Singapore, Malaysia, Australia and Europe.

Given the massive rise in cloud computing, and the accompanying demand for data storage, data centres have become a real estate asset class in itself.

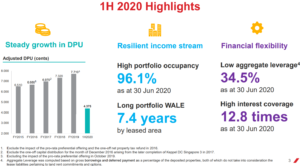

For Keppel DC REIT, that has meant a growing portfolio size as well as growing distributions. In the first half of 2020, the REIT saw net property income jump 32.1% year-on-year to S$114.2 million.

That saw Keppel DC pay out a distribution per unit (DPU) – basically the DPS – for the first half of 2020 of 4.375 Singapore cents, up an impressive 13.6% from the DPU in H1 2019. Other fundamentals also remain strong (see below).

Source: Keppel DC REIT H1 2020 earnings presentation

Over the past four years (from H1 2016 to H1 2020), Keppel DC REIT has grown its DPU at a CAGR of 7%.

If you’re looking to tap into a promising long-term trend while also accessing growing dividend income, then Keppel DC REIT could certainly be an option.

3. Venture Corp

Finally, last but not least we have Venture Corporation Ltd (SGX: V03), a leading provider of technology-focused contract manufacturing services.

It partners with many Fortune 500 companies to provide cutting-edge design and manufacturing in diverse areas from printing and imaging to medical and healthcare devices.

Venture’s latest quarterly results for the third quarter of 2020 were, understandably, slightly weaker on a year-on-year basis. Revenue and net profit both fell about 6% year-on-year to S$818.4 million and S$80.2 million respectively.

However, Venture’s unbelievably strong net cash position of S$830 million, which was up from S$713 million at the end of 2019, is supportive of its continued dividend payments.

In fact that monster net cash balance allowed Venture to raise its dividend for the first half of 2020, paying out a DPU of S$0.25. That was up 25% year-on-year from the S$0.20 it paid out in the first half of 2019.

Over the past five years, Venture’s dividend CAGR has been a respectable 7% while its shares now yield around 3.7% on a trailing 12-month basis.

Disclaimer: ProsperUs Head of Content Tim Phillips owns shares in DBS Group Holdings Ltd and Venture Corporation Ltd.