Online identify verification specialist Okta Inc (NASDAQ: OKTA) has seen phenomenal growth since listing in April 2017.

Having priced its shares at US$17 back then, Okta stock has risen more than 13-fold and now trades at around US$225 a pop.

The reason has been the integral importance of remote security and identify verification that its platform offers. Okta allows users to access a unified platform for multiple enterprise applications.

Having just released its fourth-quarter fiscal year (FY) 2021 results earlier this week, the company saw full-year revenue of US$835 million, up 43% year-on-year.

That was more than triple the revenue of US$257 million that Okta has posted in FY 2018, in three short years.

Expensive buy or a bargain?

Yet Okta’s results were overshadowed by the announcement that it would be buying identify verification competitor, Auth0, for US$6.5 billion in an all-stock deal.

As Okta’s market cap is around US$30 billion, that represents more than one-fifth of its value. Yet the market Okta and Auth0 operate in is still growing strongly.

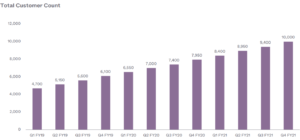

In its most recent quarter, Okta saw its total customer count grow by 26% year-on-year to hit 10,000 (see below).

Longer term, this could turn out to be an astute acquisition by Okta founder and CEO Todd McKinnon. He previously worked at Salesforce.com Inc (NYSE: CRM) under CEO Marc Benioff and seems to be following his old boss’s playbook in terms of his “growth by acquisition” approach.

Only time will tell how if the deal turns out to be a bargain. But despite the likelihood of people returning to offices this year, remote identity verification and its importance in corporate life will almost certainly keep expanding.

Source: Okta Q4 FY2021 earnings presentation

Disclaimer: ProsperUs Head of Content Tim Phillips doesn’t own shares of any companies mentioned.