Stock markets recently have been focused on the huge potential of vaccines for Covid-19. This sparked a rotation into perceived “value” stocks, such as airlines, banks and any company reliant on cross-border travel.

However, one thing that isn’t changing (after Covid-19 is finally conquered) is consumers’ taste for e-commerce. Earlier this week, Sea reported its third-quarter earnings.

The company owns the popular Southeast Asian-focused e-commerce platform Shopee and online gaming firm Garena.

Winning in e-commerce

The results were call “disappointing” and shares duly fell. If you call revenue growth of 98.7% year-on-year disappointing, then maybe you’re unreasonably expecting that sort of growth to be the norm.

However, what short-term traders fail to focus on is the extraordinary growth runway that Sea has ahead of it.

Shopee is the number one e-commerce platform in Indonesia (a country of over 250 million people) while it also ranks among the top two in most other key Southeast Asian markets.

The Southeast Asian region – home to more than 700 million people – is just at the start of its e-commerce journey.

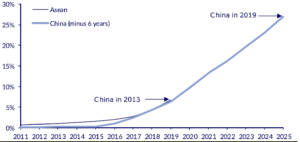

In 2019, China’s e-commerce penetration (basically the percentage of overall retail sales that took place online) was close to 30%.

In the US, this number was around 16% in 2019. How about Southeast Asia? As you can see below, it’s where China was back in 2013.

If you believe Sea is destined to be the Amazon.com Inc (NASDAQ: AMZN) of Southeast Asia then it’s US$82 billion market cap means there’s plenty more room to grow – no matter what the short-term doubters might say.

E-commerce penetration of ASEAN versus China minus six years

Source: CLSA, Euromonitor

Disclaimer: ProsperUs Head of Content Tim Phillips owns shares of Sea Ltd.